The point

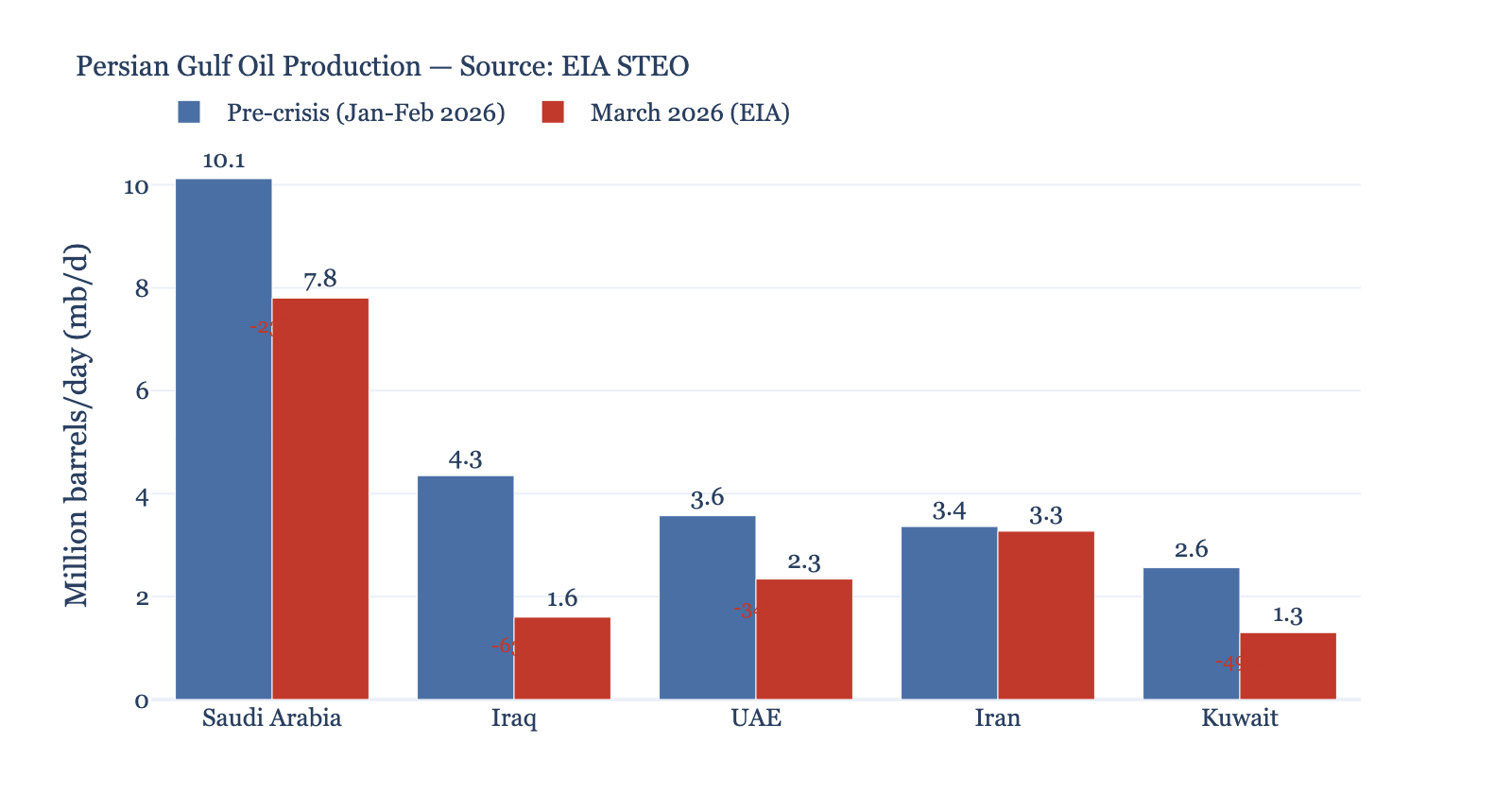

A two-week US-Iran ceasefire holds while Israel bombs Lebanon and threatens to collapse the arrangement before it stabilizes. The contradiction isn’t diplomatic but material: Trump needs Hormuz open to contain inflation, Netanyahu needs the war to continue for domestic survival, and Europe’s industrial base hangs in the balance. The ceasefire emerged not from goodwill but from energy arithmetic — with 29.6 million barrels per day still trapped behind Hormuz, and IMF projections showing global growth dragging toward recession if the blockade persists [RAG-2].

Ceasefire architecture under strain

Israel tests the boundaries while Washington calculates costs

Netanyahu announced readiness for direct talks with Lebanon “as soon as possible” while IDF strikes killed 303 Lebanese civilians Wednesday alone (Middle East Eye). The logic is transparent: keep the regional war simmering below the threshold that would force Trump to choose between his ceasefire with Iran and his support for Israel. Hezbollah lawmaker Ali Fayyad rejected direct negotiations, insisting any talks must include Iran — which exposes the fundamental contradiction in Trump’s approach (Middle East Eye).

Democratic lawmakers warned the White House that continued Israeli bombing could “reignite the regional war” (Al Jazeera). But the real constraint isn’t Congressional pressure — it’s the energy infrastructure still burning in the Gulf. Iran’s deputy foreign minister told BBC that Israeli strikes constitute a “grave violation” and the US must choose between “war and ceasefire.” The choice isn’t moral but mathematical: with refining capacity at Abqaiq, Kharg Island, and Fujairah still damaged, any return to full conflict would push oil toward $200 per barrel [RAG-5,RAG-6,RAG-7].

The first non-Iranian tanker crossed Hormuz since the ceasefire — a Gabon-flagged vessel heading to India (ANSA). This single ship represents more than symbolic progress: it tests whether Iran will honor the arrangement when Israeli strikes continue in Lebanon. Tehran claims victory while its population fears increased domestic repression (Deutsche Welle). The regime survived but emerged wounded, creating pressure for internal consolidation that could destabilize the ceasefire from within.

Negotiations begin with asymmetric leverage

Direct Israel-Lebanon talks will start next week at the State Department, according to Axios sources (ANSA). Lebanon seeks a ceasefire before negotiations begin, while Israel demands Hezbollah disarmament as the starting point. This sequencing dispute reveals the deeper dynamic: Netanyahu needs ongoing conflict to justify his political survival, while Lebanon’s government — bankrupt and dependent on external financing — cannot afford prolonged war.

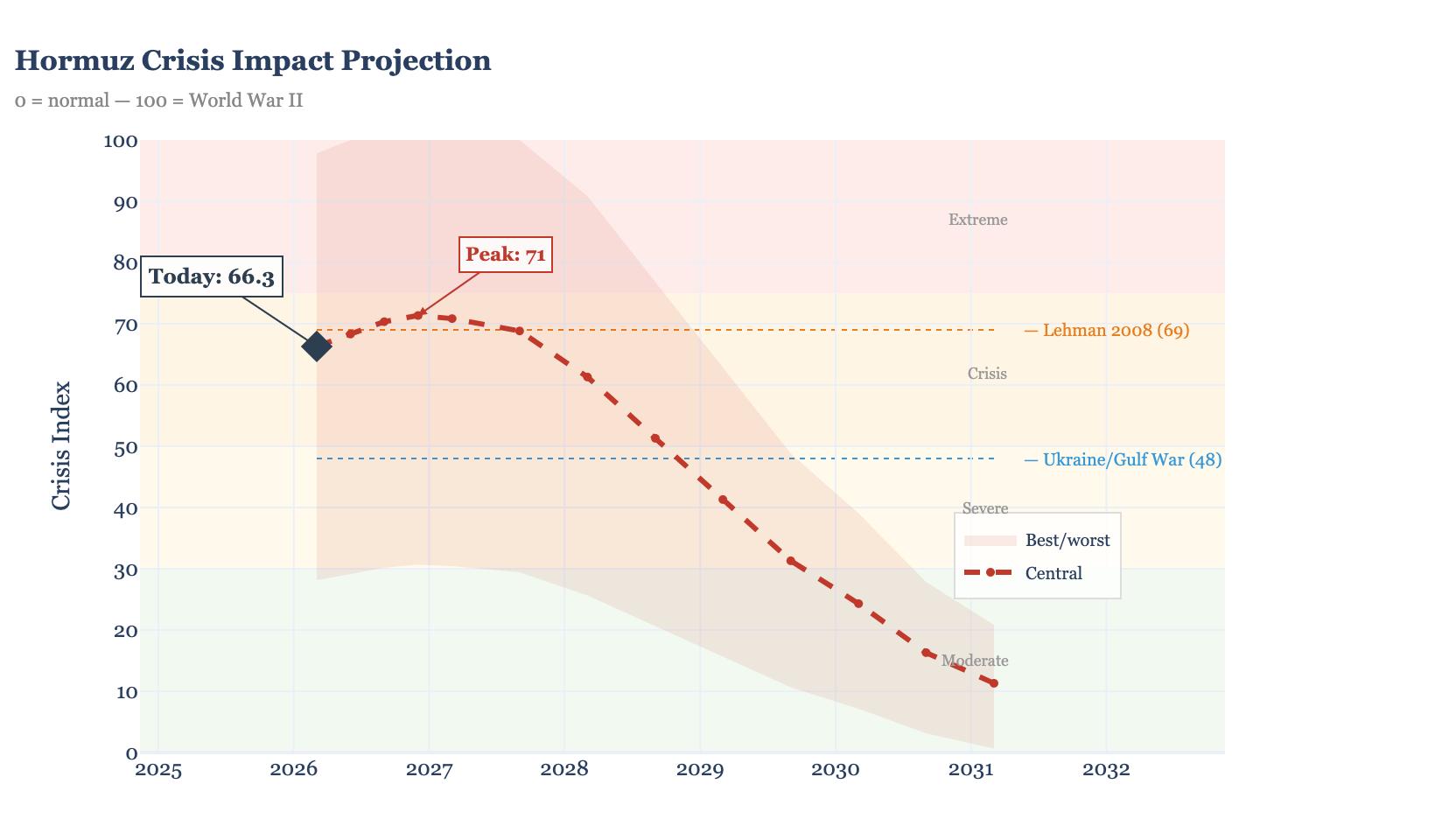

The IMF’s Kristalina Georgieva warned that the Iran war “could lead to another bout of inflation and higher interest rates” (NYT). With current damages alone, the crisis index reaches 71 by December 2026 even without new escalation [RAG-2]. Trump’s optimism about Iran deals being “within reach” (NBC interview, ANSA) reflects this constraint: his domestic economic agenda depends on energy price stability, creating leverage for Iran that doesn’t exist on the battlefield.

Industrial retreat accelerates

European manufacturing adjusts to new energy realities

Volkswagen will end EV production at its Tennessee plant, scaling back electric vehicle plans in favor of gasoline models (NYT). This reversal, framed as market preference, actually reflects supply chain disruption from the Gulf crisis. Lithium processing requires massive energy inputs, and European manufacturers face input costs that make EV production uncompetitive with Chinese alternatives.

Trump threatened 20% tariffs on European cars unless the EU removes trade barriers “soon” (SCMP). The timing links directly to the energy crisis: European manufacturers, facing higher production costs from disrupted Gulf energy flows, cannot compete on price with US production. The tariff threat provides cover for an industrial restructuring already underway due to material conditions.

Italy’s 10-year bond spread with Germany closed down to 74 basis points, with energy stocks driving Milan’s positive close (ANSA). This market movement reflects expectations that the ceasefire will hold long enough to restart Gulf production. But the arithmetic remains stark: Europe imports 15% of its oil through Hormuz, making it vulnerable to any resumption of conflict [RAG-4].

Economy & Markets

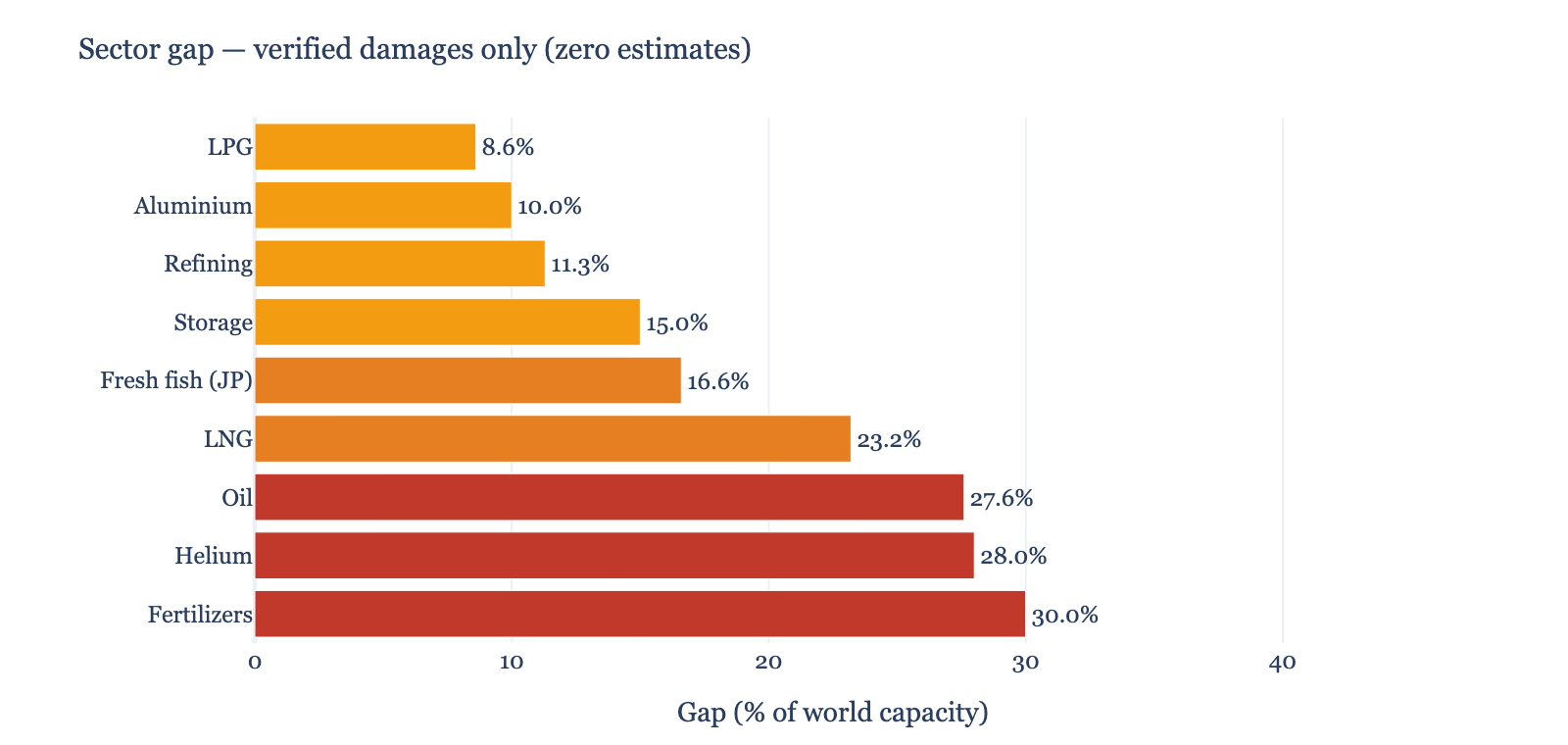

Oil markets show cautious stabilization but haven’t fully priced the fragility of current arrangements. Brent crude remains elevated as traders calculate ceasefire durability against infrastructure damage that will take months to repair. European gas prices declined on pipeline supply security, but LNG routes remain constrained with 23.2% of global capacity still affected [RAG-2].

Italian BTPs outperformed German Bunds as energy sector strength drove Milan higher. ENI and Leonardo led gains, reflecting market expectations of Gulf production resumption. But the 74 basis point spread still prices significant political risk premium.

The first Hormuz crossing by a non-Iranian tanker provides concrete evidence the waterway is reopening, but single-digit vessel counts remain far below the normal 40+ daily transits required for global energy security.

Weak signals

Universal Music Group faces a €55 billion bid from hedge fund manager Bill Ackman, highlighting how energy crisis capital seeks stable revenue streams in entertainment assets while manufacturing faces input cost pressures (Financial Times).

LA28 Olympics ticket sales exceeded all previous domestic demand, suggesting American consumer confidence remains strong despite geopolitical tensions — or perhaps because of expectation that conflicts will resolve before 2028.

Three Russian submarines conducted month-long “covert operations” near UK undersea cables and pipelines, according to British Defence Secretary John Healey, who suggested Putin wants the West “distracted by the Middle East” (NYT, SCMP). Moscow’s submarine activity during the Gulf crisis indicates strategic coordination between rival powers.

Key takeaway

The US-Iran ceasefire holds because both sides need it, but for different reasons that create structural instability. Trump requires energy price stability for his domestic agenda. Iran needs time to consolidate after surviving regime-threatening bombardment. Netanyahu needs controlled conflict to maintain power. These contradictory requirements cannot be reconciled indefinitely. The ceasefire’s duration depends on how quickly Gulf energy infrastructure comes back online — and whether Israel’s bombing of Lebanon crosses thresholds that force Trump to choose between his Iran deal and his Israel relationship.

Worth reading

- IMF Global Economic Outlook update on Iran war impact

- EIA weekly petroleum status report for Gulf production data

- UKMTO maritime security updates for Hormuz shipping resumption

- Israeli Knesset proceedings on Lebanon negotiation authorization

- Federal Reserve meeting minutes on inflation expectations amid energy volatility

—

This publication provides analysis and information for educational purposes only. It does not constitute investment advice, a personal recommendation, or an offer to buy or sell any financial instrument. The author is not a registered investment advisor. Past statistical patterns do not guarantee future results.

Orizzonti Quotidiani — For the Future | orizzonti.news

10 April 2026 — 03:01 JST · 20:01 CEST · 14:01 EST