The point

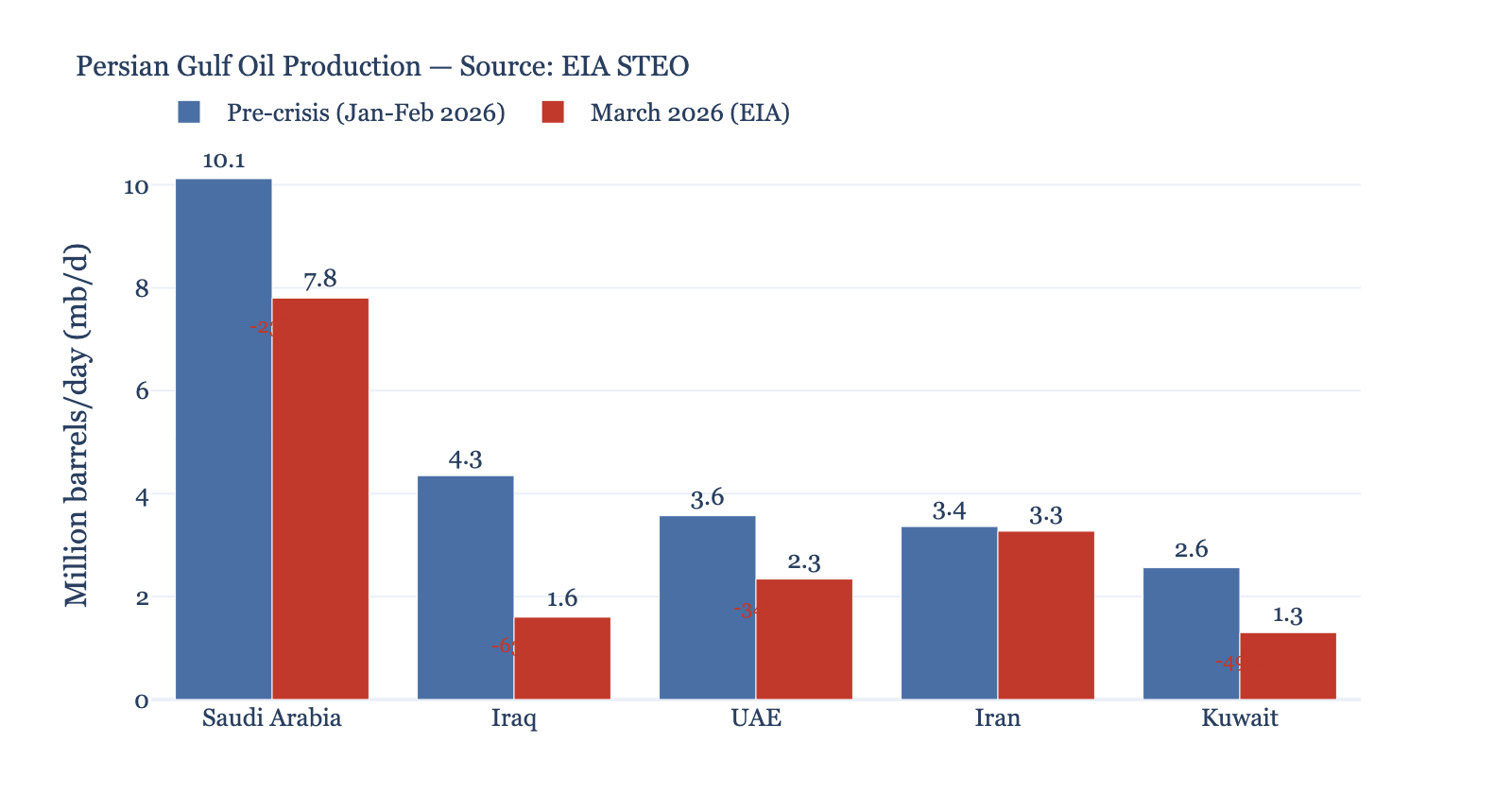

Vice President JD Vance lands in Pakistan today as Washington and Tehran attempt their first direct negotiations—not to resolve Middle Eastern contradictions, but to manage the collapse of American energy dominance. With 22 million barrels trapped daily behind Hormuz and global fuel costs forcing airlines to cancel flights from Hong Kong to Bangkok, the talks reveal which empire can least afford prolonged economic warfare. Markets rally on ceasefire hopes while EIA data shows Gulf production down 7.6 million barrels per day. The contradiction: both powers negotiate from positions they cannot sustain.

Capital flows around the blockade

Airlines capitulate to fuel reality

Cathay Pacific cuts 2% of flights through June as jet fuel prices surge beyond operational viability (Straits Times). Thai travelers pay premium rates for New Year journeys home, accepting transport costs that would have halted travel entirely six months ago (SCMP). The arithmetic is simple: carriers absorb losses until shareholders revolt, then pass costs to consumers until demand destruction begins. Neither has occurred yet—revealing how far fuel prices can climb before the real economic adjustment starts.

Hungary’s energy dependency votes

Tomorrow’s Hungarian election carries implications beyond Viktor Orbán’s 14-year rule. With 8.1 million voters deciding between Orbán’s Russia alignment and opposition leader Péter Magyar’s Western pivot, the outcome determines whether Putin retains his sole EU ally during the Gulf crisis (France 24). Trump’s public endorsement of Orbán signals American recognition that European energy flows require Russian cooperation—even as Washington negotiates Iranian oil access. The contradiction exposes both empires’ energy vulnerability.

Pakistan extracts mediation fees

Islamabad hosts today’s talks not from diplomatic neutrality but economic necessity. Prime Minister Shehbaz Sharif meets both Vance and Iranian delegates knowing Pakistan’s $350 billion external financing needs require American and Chinese backing simultaneously (NHK, Financial Times). The mediation role generates strategic rent: promises of IMF support, CPEC project continuation, and Gulf remittance flows. Pakistan’s leverage derives from geographical necessity—the only regional power acceptable to both Washington and Tehran.

Economy & Markets

S&P 500 records worst performance across Trump presidencies as energy sector volatility overwhelms tax cut optimism (Financial Times). The index reflects market confusion: oil service stocks rally on supply constraints while transport and manufacturing shares decline on input cost projections. Iranian asset unfreezing reports drive crude futures down 3% before US denials restore gains (Reuters, ANSA). The whipsaw reveals how quickly energy geopolitics now moves capital allocation.

Hong Kong property landlords seek 3-year compliance delays on subdivided housing standards as construction costs surge with material shortages (SCMP). Thailand increases essential goods allowances for “vulnerable groups”—bureaucratic language for populations facing food inflation beyond subsistence thresholds (Straits Times).

Weak signals

Hezbollah’s surprising endurance reveals Iranian weapons stockpiling exceeded Israeli intelligence estimates. The group’s sustained rocket capacity despite targeted assassinations suggests supply chains through Syria remained operational longer than Jerusalem calculated (New York Times).

Djibouti’s election delivers President Ismaïl Omar Guelleh a sixth term with 97.8% support, extending 27-year rule over the Red Sea chokepoint (BBC). Opposition boycotts signal internal consent exhaustion, but Guelleh controls Chinese naval facility access and US drone base operations simultaneously.

Chinese-British-Kenyan rail cooperation proceeds despite Western sanctions pressure, demonstrating how infrastructure needs override geopolitical preferences when economic returns remain positive (SCMP).

Local effects

Italy: Vinitaly opens tomorrow with 4,000 companies and five ministers attending, showcasing agricultural exports while wine transport costs surge 15% on fuel price spikes (ANSA). Amazon workers at Passo Corese sign “historic agreement” limiting remote surveillance—labor organizing accelerates as energy costs squeeze corporate margins.

Japan: Tokyo markets surge 2,800 points on ceasefire speculation before retreating on US asset denial. Women’s basketball Denso reaches championship finals, diverting attention from Strait crisis impacts on automotive supply chains.

Key takeaway

Washington and Tehran negotiate because both economies cannot sustain current trajectories. America’s energy independence rhetoric crumbles when Gulf disruption forces diplomatic engagement with sanctioned regimes. Iran’s revolutionary rhetoric softens when oil revenue becomes existential necessity. The talks succeed only if both sides find face-saving formulas for mutual retreat—or fail when neither can afford the concessions required.

Worth reading

- Financial Times: JD Vance arrives in Pakistan for ‘positive’ peace talks with Iran

- Reuters: US agrees to unfreeze Iranian assets in foreign banks

- SCMP: Cathay Pacific to cut flights from mid-May as jet fuel prices surge

- France 24: An Orban loss could be the turning point Putin fears

- New York Times: In New War, Hezbollah Defies Notion It Was Crippled

—

This publication provides analysis and information for educational purposes only. It does not constitute investment advice, a personal recommendation, or an offer to buy or sell any financial instrument. The author is not a registered investment advisor. Past statistical patterns do not guarantee future results.

Orizzonti Quotidiani — For the Future | orizzonti.news

11 April 2026 — 20:03 JST · 13:03 CEST · 07:03 EST